History of money

| Numismatics |

|---|

.png) |

| Currency |

| Circulating currencies |

|

| Local currencies |

| Fictional currencies |

| History |

| Historical currencies |

| Byzantine |

| Medieval currencies |

| Production |

| Exonumia |

| Notaphily |

| Scripophily |

|

The history of money concerns the development of means of carrying out transactions involving a medium of exchange. Money is any clearly identifiable object of value that is generally accepted as payment for goods and services and repayment of debts within a market or which is legal tender within a country.

Many things have been used as medium of exchange in markets including, for example, livestock and sacks of cereal grain (from which the Shekel is derived) – things directly useful in themselves, but also sometimes merely attractive items such as cowry shells or beads were exchanged for more useful commodities. Precious metals, from which early coins were made, fall into both categories.

In modern times the broader concept of "money" includes other forms of money such as bank accounts. The history of money also includes items such as credit cards.

Numismatics is the study of physical money such as coins and paper money.

Non-monetary exchange

Barter

In Politics Book 1:9[1] (c.350 B.C.) the Greek philosopher Aristotle contemplated on the nature of money. He considered that every object has two uses, the first being the original purpose for which the object was designed, and the second possibility is to conceive of the object as an item to sell or barter.[2] The assignment of monetary value to an otherwise insignificant object such as a coin or promissory note arises as people and their trading associate evolve a psychological capacity to place trust in each other and in external authority within barter exchange.[3][4]

With barter, an individual possessing any surplus of value, such as a measure of grain or a quantity of livestock could directly exchange that for something perceived to have similar or greater value or utility, such as a clay pot or a tool. The capacity to carry out barter transactions is limited in that it depends on a coincidence of wants. The seller of food grain has to find the buyer who wants to buy grain and who also could offer in return something the seller wants to buy. There is no agreed standard measure into which both seller and buyer could exchange commodities according to their relative value of all the various goods and services offered by other potential barter partners.

Criticisms

David Kinley considers the theory of Aristotle to be flawed because the philosopher probably lacked sufficient understanding of the ways and practices of primitive communities, and so may have formed his opinion from personal experience and conjecture.

In his book Debt: The First 5000 Years, anthropologist David Graeber argues against the suggestion that money was invented to replace barter. The problem with this version of history, he suggests, is the lack of any supporting evidence. His research indicates that "gift economies" were common, at least at the beginnings of the first agrarian societies, when humans used elaborate credit systems. Graeber proposes that money as a unit of account was invented the moment when the unquantifiable obligation "I owe you one" transformed into the quantifiable notion of "I owe you one unit of something". In this view, money emerged first as credit and only later acquired the functions of a medium of exchange and a store of value.[5][6]

Gift economy

In a gift economy, valuable goods and services are regularly given without any explicit agreement for immediate or future rewards (i.e. there is no formal quid pro quo).[7] Ideally, simultaneous or recurring giving serves to circulate and redistribute valuables within the community.

There are various social theories concerning gift economies. Some consider the gifts to be a form of reciprocal altruism. Another interpretation is that implicit "I owe you" debt[8] and social status are awarded in return for the "gifts".[9] Consider for example, the sharing of food in some hunter-gatherer societies, where food-sharing is a safeguard against the failure of any individual's daily foraging. This custom may reflect altruism, it may be a form of informal insurance, or may bring with it social status or other benefits.

Emergence of money

Anatolian obsidian as a raw material for stone-age tools was distributed as early as 15,000 BCE, with organized trade occurring in the 9th millennium. (Cauvin;Chataigner 1998)[10] In Sardinia, one of the four main sites for sourcing the material deposits of obsidian within the Mediterranean, trade in this was replaced in the 3rd millennium by trade in copper and silver.[11][12][13][14]

As early as 9000 BCE both grain and cattle were used as money or as barter (Davies) (the first grain remains found, considered to be evidence of pre-agricultural practice date to 17,000 BCE).[15][16][17]

In the earliest instances of trade with money, the things with the greatest utility and reliability in terms of re-use and re-trading of these things (their marketability), determined the nature of the object or thing chosen to exchange. So as in agricultural societies, things needed for efficient and comfortable employment of energies for the production of cereals and the like were the most easy to transfer to monetary significance for direct exchange. As more of the basic conditions of the human existence were met to the satisfaction of human needs,[18] so the division of labour increased to create new activities for the use of time to solve more advanced concerns. As people's needs became more refined, indirect exchange became more likely as the physical separation of skilled labourers (suppliers) from their prospective clients (demand) required the use of a medium common to all communities, to facilitate a wider market.[19][20]

Aristotle's opinion of the creation of money[4] as a new thing in society is:

When the inhabitants of one country became more dependent on those of another, and they imported what they needed, and exported what they had too much of, money necessarily came into use.[21]

The worship of Moneta is recorded by Livy with the temple built in the time of Rome 413 (123); a temple consecrated to the same god was built in the earlier part of the fourth century (perhaps the same temple).[22][23][24] The temple contained the mint of Rome for a period of four centuries.[25][26]

The Code of Hammurabi, the best preserved ancient law code, was created ca. 1760 BCE (middle chronology) in ancient Babylon. It was enacted by the sixth Babylonian king, Hammurabi. Earlier collections of laws include the code of Ur-Nammu, king of Ur (ca. 2050 BCE), the Code of Eshnunna (ca. 1930 BCE) and the code of Lipit-Ishtar of Isin (ca. 1870 BCE).[27] These law codes formalized the role of money in civil society. They set amounts of interest on debt... fines for 'wrongdoing'... and compensation in money for various infractions of formalized law.

The Mesopotamian civilization developed a large scale economy based on commodity money. The Babylonians and their neighboring city states later developed the earliest system of economics as we think of it today, in terms of rules on debt,[8] legal contracts and law codes relating to business practices and private property. Money was not only an emergence, it was a necessity.[28][29]

Early usage

The earliest means of storage are thought to be money-boxes (θησαυροί[30]) made similar to the construction of a bee-hive,[31][32] as of the Mycenae tombs of 1550–1500 BCE.[33][34][35]

Cattle were used as an early form of currency from 9,000 BCE onward (Davies 1996 & 1999).[36][37] Both the animal and the manure produced were valuable; animals are recorded as being used as payment as in Roman law where fines were paid in oxen and sheep (Rollin 1836)[38][39][40] and within the Iliad and Odyssey, attesting to a value c. 850–800 BCE (Evans & Schmalensee 2005).[41][42]

It has long been assumed that metals, where available, were favored for use as proto-money over such commodities as cattle, cowry shells, or salt, because metals are at once durable, portable, and easily divisible.[43] The use of gold as proto-money has been traced back to the fourth millennium BCE when the Egyptians used gold bars of a set weight as a medium of exchange, as had been done earlier in Mesopotamia with silver bars.

The first mention of the use of money within the Bible is within the Book of Genesis[44] in reference to criteria of the circumcision of a bought slave. Later, the Cave of Machpelah is purchased (with silver[45][46]) by Abraham,[47] during a period dated as being the beginning of the twentieth century BCE,[48] some-time recent to 1900 BCE[49] (after 1985).[50] The currency was also in use amongst the Philistine people of the same time-period.[51]

The shekel was an ancient unit[52] used in Mesopotamia around 3000 BCE to define both a specific weight of barley and equivalent amounts of materials such as silver, bronze and copper. The use of a single unit to define both mass and currency was a similar concept to the British pound, which was originally defined as a one-pound mass of silver.

Transactions which used precious metals as currency were carried out by dividing (clipping;Greek κέρδος) the material into an amount corresponding to the perceived value of the item being purchased. From this one might understand how coinage was imagined from the small metallic clippings (of silver[53][54][55]) resulting from trade exchanges.[56] The word used in Thucydides writings History for money is χρήματα ("chremata"), translated in some contexts as "goods" or "property", although with a wider ranging possible applicable usage, having a definite meaning "valuable things".[57][58][59][60]

The Indus Valley Civilisation of India dates back between 2500 BCE and 1750 BCE. There, however, is no consensus on whether the seals excavated from the sites were in fact coins. The first gold coins of the Grecian age were struck in Lydia at a time approximated to the year 700 BCE[61] The talent[52][62] in use during the periods of Grecian history both before and during the time of the life of Homer, weighed between 8.42 and 8.75 grammes.[63] (p. 3 – Seltman)

Commodity money

Bartering has several problems, most notably that it requires a "coincidence of wants". For example, if a wheat farmer needs what a fruit farmer produces, a direct swap is impossible as seasonal fruit would spoil before the grain harvest. A solution is to trade fruit for wheat indirectly through a third, "intermediate", commodity: the fruit is exchanged for the intermediate commodity when the fruit ripens. If this intermediate commodity doesn't perish and is reliably in demand throughout the year (e.g. copper, gold, or wine) then it can be exchanged for wheat after the harvest. The function of the intermediate commodity as a store-of-value can be standardized into a widespread commodity money, reducing the coincidence of wants problem. By overcoming the limitations of simple barter, a commodity money makes the market in all other commodities more liquid.

Many cultures around the world eventually developed the use of commodity money. Ancient China, Africa, and India used cowry shells. Trade in Japan's feudal system was based on the koku – a unit of rice. The shekel was an ancient unit of weight and currency. The first usage of the term came from Mesopotamia circa 3000 BC and referred to a specific weight of barley, which related other values in a metric such as silver, bronze, copper etc. A barley/shekel was originally both a unit of currency and a unit of weight.[64]

Wherever trade is common, barter systems usually lead quite rapidly to several key goods being imbued with monetary properties. In the early British colony of New South Wales, rum emerged quite soon after settlement as the most monetary of goods. When a nation is without a currency it commonly adopts a foreign currency. In prisons where conventional money is prohibited, it is quite common for cigarettes to take on a monetary quality. Contrary to popular belief, precious metals have rarely been used outside of large societies. Gold, in particular, is sufficiently scarce that it has only been used as a currency for a few relatively brief periods in history.

Standardized coinage

From approximately 1000 BC money in the shape of small knives and spades made of bronze were in use in China during the Zhou dynasty, with cast bronze replicas of cowrie shells in use before this. The first manufactured coins seems to have taken place separately in India, China, and in cities around the Aegean sea between 700 and 500 BC.[65] While these Aegean coins were stamped (heated and hammered with insignia), the Indian coins (from the Ganges river valley) were punched metal disks, and Chinese coins (first developed in the Great Plain) were cast bronze with holes in the center to be strung together. The different forms and metallurgical process implies a separate development.[66]

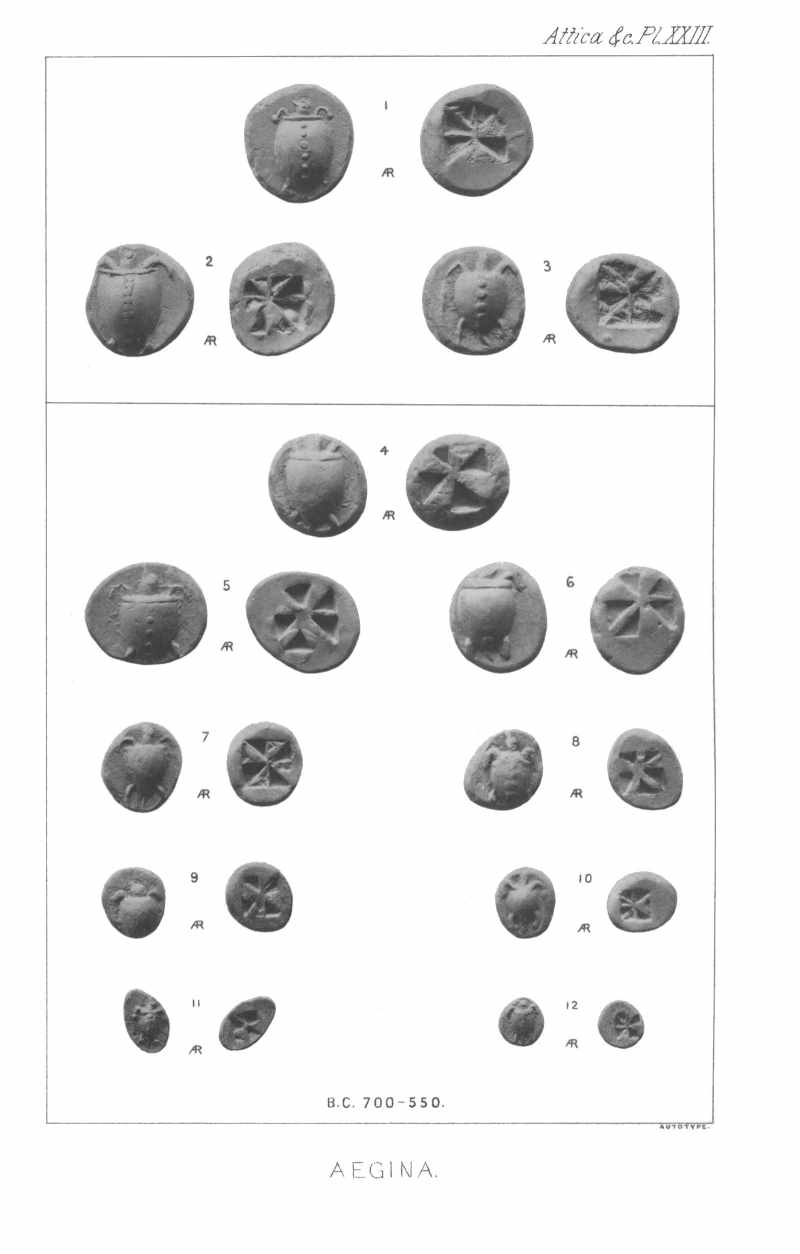

The first ruler in the Mediterranean known to have officially set standards of weight and money was Pheidon.[67] Minting occurred in the latter parts of the 7th century amongst the cities of Grecian Asia Minor, spreading to Aegean parts of the Greek islands and the south of Italy by 500 BC.[26] The first stamped money (having the mark of some authority in the form of a picture or words) can be seen in the Bibliothèque Nationale of Paris. It is an electrum stater of a turtle coin, coined at Aegina island. This coin[68] dates about 700 BC.[69]

Other coins made of Electrum (a naturally occurring alloy of silver and gold) were manufactured on a larger scale about 650 BC in Lydia (on the coast of what is now Turkey).[70] Similar coinage was adopted and manufactured to their own standards in nearby cities of Ionia, including Mytilene and Phokaia (using coins of Electrum) and Aegina (using silver) during the 6th century BC. and soon became adopted in mainland Greece itself, and the Persian Empire (after it incorporated Lydia in 547 BC).

The use and export of silver coinage, along with soldiers paid in coins, contributed to the Athenian Empire's 5th century BC, dominance of the region. The silver used was mined in southern Attica at Laurium and Thorikos by a huge workforce of slave labour. A major silver vein discovery at Laurium in 483 BC led to the huge expansion of the Athenian military fleet.

It was the discovery of the touchstone which led the way for metal-based commodity money and coinage. Any soft metal can be tested for purity on a touchstone, allowing one to quickly calculate the total content of a particular metal in a lump. Gold is a soft metal, which is also hard to come by, dense, and storable. As a result, monetary gold spread very quickly from Asia Minor, where it first gained wide usage, to the entire world.

Using such a system still required several steps and mathematical calculation. The touchstone allows one to estimate the amount of gold in an alloy, which is then multiplied by the weight to find the amount of gold alone in a lump. To make this process easier, the concept of standard coinage was introduced. Coins were pre-weighed and pre-alloyed, so as long as the manufacturer was aware of the origin of the coin, no use of the touchstone was required. Coins were typically minted by governments in a carefully protected process, and then stamped with an emblem that guaranteed the weight and value of the metal. It was, however, extremely common for governments to assert that the value of such money lay in its emblem and thus to subsequently reduce the value of the currency by lowering the content of valuable metal.

Gold and silver were used as the most common form of money throughout history. In many languages, such as Spanish, French, and Italian, the word for silver is still directly related to the word for money. Although gold and silver were commonly used to mint coins, other metals were used. For instance, Ancient Sparta minted coins from iron to discourage its citizens from engaging in foreign trade.[71] In the early seventeenth century Sweden lacked more precious metal and so produced "plate money", which were large slabs of copper approximately 50 cm or more in length and width, appropriately stamped with indications of their value.

Gold coinage began to be minted again in Europe in the thirteenth century. Frederick the II is credited with having re-introduced the metal to currency during the time of the Crusades. During the fourteenth century Europe had en masse converted from use of silver in currency to minting of gold.[72][73] Vienna transferred from minting silver to instead gold during 1328.[72]

Metal based coins had the advantage of carrying their value within the coins themselves – on the other hand, they induced manipulations: the clipping of coins in the attempt to get and recycle the precious metal. A greater problem was the simultaneous co-existence of gold, silver and copper coins in Europe. English and Spanish traders valued gold coins more than silver coins, as many of their neighbors did, with the effect that the English gold-based guinea coin began to rise against the English silver based crown in the 1670s and 1680s. Consequently, silver was ultimately pulled out of England for dubious amounts of gold coming into the country at a rate no other European nation would share. The effect was worsened with Asian traders not sharing the European appreciation of gold altogether — gold left Asia and silver left Europe in quantities European observers like Isaac Newton, Master of the Royal Mint observed with unease.[74]

Stability came into the system with national Banks guaranteeing to change money into gold at a promised rate; it did, however, not come easily. The Bank of England risked a national financial catastrophe in the 1730s when customers demanded their money be changed into gold in a moment of crisis. Eventually London's merchants saved the bank and the nation with financial guarantees.

Another step in the evolution of money was the change from a coin being a unit of weight to being a unit of value. A distinction could be made between its commodity value and its specie value. The difference is these values is seigniorage.[75]

Trade bills of exchange

Bills of exchange became prevalent with the expansion of European trade toward the end of the Middle Ages. A flourishing Italian wholesale trade in cloth, woolen clothing, wine, tin and other commodities was heavily dependent on credit for its rapid expansion. Goods were supplied to a buyer against a bill of exchange, which constituted the buyer's promise to make payment at some specified future date. Provided that the buyer was reputable or the bill was endorsed by a credible guarantor, the seller could then present the bill to a merchant banker and redeem it in money at a discounted value before it actually became due. The main purpose of these bills nevertheless was, that traveling with cash was particularly dangerous at the time. A deposit could be made with a banker in one town, in turn a bill of exchange was handed out, that could be redeemed in another town.

These bills could also be used as a form of payment by the seller to make additional purchases from his own suppliers. Thus, the bills – an early form of credit – became both a medium of exchange and a medium for storage of value. Like the loans made by the Egyptian grain banks, this trade credit became a significant source for the creation of new money. In England, bills of exchange became an important form of credit and money during last quarter of the 18th century and the first quarter of the 19th century before banknotes, checks and cash credit lines were widely available.[76]

Tallies

The acceptance of symbolic forms of money opened up vast new realms for human creativity. A symbol could be used to represent something of value that was available in physical storage somewhere else in space, such as grain in the warehouse. It could also be used to represent something of value that would be available later in time, such as a promissory note or bill of exchange, a document ordering someone to pay a certain sum of money to another on a specific date or when certain conditions have been fulfilled.

In the 12th century, the English monarchy introduced an early version of the bill of exchange in the form of a notched piece of wood known as a tally stick. Tallies originally came into use at a time when paper was rare and costly, but their use persisted until the early 19th Century, even after paper forms of money had become prevalent. The notches were used to denote various amounts of taxes payable to the crown. Initially tallies were simply used as a form of receipt to the tax payer at the time of rendering his dues. As the revenue department became more efficient, they began issuing tallies to denote a promise of the tax assessee to make future tax payments at specified times during the year. Each tally consisted of a matching pair – one stick was given to the assessee at the time of assessment representing the amount of taxes to be paid later and the other held by the Treasury representing the amount of taxes be collected at a future date.

The Treasury discovered that these tallies could also be used to create money. When the crown had exhausted its current resources, it could use the tally receipts representing future tax payments due to the crown as a form of payment to its own creditors, who in turn could either collect the tax revenue directly from those assessed or use the same tally to pay their own taxes to the government. The tallies could also be sold to other parties in exchange for gold or silver coin at a discount reflecting the length of time remaining until the taxes was due for payment. Thus, the tallies became an accepted medium of exchange for some types of transactions and an accepted medium for store of value. Like the girobanks before it, the Treasury soon realized that it could also issue tallies that were not backed by any specific assessment of taxes. By doing so, the Treasury created new money that was backed by public trust and confidence in the monarchy rather than by specific revenue receipts.[77]

Goldsmith bankers

Goldsmiths in England had been craftsmen, bullion merchants, money changers and money lenders since the 16th century. But they were not the first to act as financial intermediates; in the early 17th century, the scriveners were the first to keep deposits for the express purpose of relending them.[78] Merchants and traders had amassed huge hoards of gold and entrusted their wealth to the Royal Mint for storage. In 1640 King Charles I seized the private gold stored in the mint as a forced loan (which was to be paid back over time). Thereafter merchants preferred to store their gold with the goldsmiths of London, who possessed private vaults, and charged a fee for that service. In exchange for each deposit of precious metal, the goldsmiths issued receipts certifying the quantity and purity of the metal they held as a bailee (i.e. in trust). These receipts could not be assigned (only the original depositor could collect the stored goods). Gradually the goldsmiths took over the function of the scriveners of relending on behalf of a depositor and also developed modern banking practices; promissory notes were issued for money deposited which by custom and/or law was a loan to the goldsmith,[79] i.e. the depositor expressly allowed the goldsmith to use the money for any purpose including advances to his customers. The goldsmith charged no fee, or even paid interest on these deposits. Since the promissory notes were payable on demand, and the advances (loans) to the goldsmith's customers were repayable over a longer time period, this was an early form of fractional reserve banking. The promissory notes developed into an assignable instrument, which could circulate as a safe and convenient form of money backed by the goldsmith's promise to pay.[80] Hence goldsmiths could advance loans in the form of gold money, or in the form of promissory notes, or in the form of checking accounts.[81] Gold deposits were relatively stable, often remaining with the goldsmith for years on end, so there was little risk of default so long as public trust in the goldsmith's integrity and financial soundness was maintained. Thus, the goldsmiths of London became the forerunners of British banking and prominent creators of new money based on credit.

Demand deposits

The primary business of the early merchant banks was promotion of trade. The new class of commercial banks made accepting deposits and issuing loans their principal activity. They lend the money they received on deposit. They created additional money in the form of new bank notes. The money they created was partially backed by gold, silver or other assets and partially backed only by public trust in the institutions that created it.

Demand deposits are funds that are deposited in bank accounts and are available for withdrawal at the discretion of the depositor. The withdrawal of funds from the account does not require contacting or making any type of prior arrangements with the bank or credit union. As long as the account balance is sufficient to cover the amount of the withdrawal, and the withdrawal takes place in accordance with procedures set in place by the financial institution, the funds may be withdrawn on demand

Banknotes

.jpg)

Paper money was introduced in Song Dynasty China during the 11th century.[82] The development of the banknote began in the seventh century, with local issues of paper currency. Its roots were in merchant receipts of deposit during the Tang Dynasty (618–907), as merchants and wholesalers desired to avoid the heavy bulk of copper coinage in large commercial transactions.[83][84][85] The issue of credit notes is often for a limited duration, and at some discount to the promised amount later. The jiaozi nevertheless did not replace coins during the Song Dynasty; paper money was used alongside the coins. The central government soon observed the economic advantages of printing paper money, issuing a monopoly right of several of the deposit shops to the issuance of these certificates of deposit.[86] By the early 12th century, the amount of banknotes issued in a single year amounted to an annual rate of 26 million strings of cash coins.[87]

In the 13th century, paper money became known in Europe through the accounts of travelers, such as Marco Polo and William of Rubruck.[88] Marco Polo's account of paper money during the Yuan Dynasty is the subject of a chapter of his book, The Travels of Marco Polo, titled "How the Great Kaan Causeth the Bark of Trees, Made into Something Like Paper, to Pass for Money All Over his Country."[89] In medieval Italy and Flanders, because of the insecurity and impracticality of transporting large sums of money over long distances, money traders started using promissory notes. In the beginning these were personally registered, but they soon became a written order to pay the amount to whoever had it in their possession.[90] These notes can be seen as a predecessor to regular banknotes.[91] The first European banknotes were issued by Stockholms Banco, a predecessor of the Bank of Sweden, in 1661.[92] These replaced the copper-plates being used instead as a means of payment,[93] although in 1664 the bank ran out of coins to redeem notes and ceased operating in the same year.

Inspired by the success of the London goldsmiths, some of which became the forerunners of great English banks, banks began issuing paper notes quite properly termed ‘banknotes’ which circulated in the same way that government issued currency circulates today. In England this practice continued up to 1694. Scottish banks continued issuing notes until 1850. In USA, this practice continued through the 19th Century, where at one time there were more than 5000 different types of bank notes issued by various commercial banks in America. Only the notes issued by the largest, most creditworthy banks were widely accepted. The script of smaller, lesser known institutions circulated locally. Farther from home it was only accepted at a discounted rate, if it was accepted at all. The proliferation of types of money went hand in hand with a multiplication in the number of financial institutions.

These banknotes were a form of representative money which could be converted into gold or silver by application at the bank. Since banks issued notes far in excess of the gold and silver they kept on deposit, sudden loss of public confidence in a bank could precipitate mass redemption of banknotes and result in bankruptcy.

The use of bank notes issued by private commercial banks as legal tender has gradually been replaced by the issuance of bank notes authorized and controlled by national governments. The Bank of England was granted sole rights to issue banknotes in England after 1694. In the USA, the Federal Reserve Bank was granted similar rights after its establishment in 1913. Until recently, these government-authorized currencies were forms of representative money, since they were partially backed by gold or silver and were theoretically convertible into gold or silver.

Cryptocurrencies

The latest development in money uses cryptology to ensure trust & fungibility in a theoretically tamper-proof decentralized ledger called a blockchain. The first successful cryptocurrency is Bitcoin, and since its inception hundreds of other crypto-backed coins have been introduced. The system is more akin to tally sticks and other types of ledger-based money than to coinage, despite the name.

See also

References

- ↑ S Meikle Aristotle on Money Phronesis Vol. 39, No. 1 (1994), pp. 26–44 Retrieved 2012-06-05

- ↑ Aristotle Politics Translated by Benjamin Jowett MIT University

- ↑ N K Lewis (2001). Gold: The Once and Future Money. John Wiley & Sons, 4 May 2007. ISBN 0470047666. Retrieved 2012-06-04.

- 1 2 D Kinley (2001). Money: A Study of the Theory of the Medium of Exchange. Simon Publications LLC, 1 September 2003. ISBN 193251211X. Retrieved 2012-06-04.

- ↑ Graeber, David (12 July 2011). Debt: The First 5,000 Years. ISBN 1-933633-86-7.

- ↑ Graeber, David (26 August 2011). "What is Debt? – An Interview with Economic Anthropologist David Graeber".

- ↑ Cheal, David J (1988). "1". The Gift Economy. New York: Routledge. pp. 1–19. ISBN 0-415-00641-4. Retrieved 2009-06-18.

- 1 2 "What is Debt? – An Interview with Economic Anthropologist David Graeber". Naked Capitalism.

- ↑ Gifford Pinchot – The Gift Economy. Context.org (2000-06-29). Retrieved on 2011-02-10.

- ↑ Volume 3 of Proceedings of the 6th International Congress of the Archaeology of the Ancient Near East: 5–10 May 2009 6 ICAANE Licia Romano Otto Harrassowitz Verlag, 2010 ISBN 3447062177 Retrieved 2012-06-09

- ↑ N H Demand The Mediterranean Context of Early Greek History John Wiley & Sons 2012 – Retrieved 2012-06-09

- ↑ secondary- + + + + Retrieved 2012-06-09

- ↑ John Bintliff 2012 The Complete Archaeology of Greece: From Hunter-Gatherers to the 20th Century A.D. John Wiley & Sons, 19 mars 2012 John Wiley & Sons, 19 mars 2012 ISBN 1118255194 Retrieved 2012-06-09

- ↑ (secondary) – S King & F Darabont-StevenKing.com The Official website → Retrieved 2012-06-09

- ↑ G A Slafer – Barley Science: Recent Advances from Molecular Biology to Agronomy of Yield and Quality p.1 Routledge, 12 March 2002 ISBN 1560229101 Retrieved 2012-06-17

- ↑ G Davies, J H Bank – A history of money: from ancient times to the present day University of Wales Press, 2002 – Retrieved 2012-05-17

- ↑ J Huerta de Soto – 1998 (translated by M.A.Stroup 2012). Money, Bank Credit, and Economic Cycles. Ludwig von Mises Institute. ISBN 1610161890. Retrieved 2012-06-15.

- ↑ Abraham Maslow : Maslow's Hierarchy of Needs in Richard Gross – Psychology: The Science of Mind and Behaviour ISBN 144410831X

- ↑ Ludwig Von Mises. The Theory of Money and Credit. Ludwig von Mises Institute, 2009. ISBN 1933550554. Retrieved 2012-10-06.

- ↑ K.Marx, F.Engels The Communist Manifesto ISBN 1406851744 Retrieved 2012-06-04

- ↑ Aristotle

- ↑ D Harper – etymology online Retrieved 2012-06-09

- ↑ P Bayle, P Desmaizeaux, A Tricaud, A Gaudin – The dictionary historical and critical of Mr. Peter Bayle, Volume 3 Printed for J. J. and P. Knapton; D. Midwinter; J. Brotherton; A. Bettesworth and C. Hitch ... [and 25 others], 1736 – Retrieved 2012-06-09

- ↑ P B Harvey, C E Schultz Religion in Republican Italy Cambridge University Press, 2006 -ISBN 052186366X Retrieved 2012-06-09

- ↑ Rome Reborn – University of Virginia – Institute for Advanced Technology in the Humanities Retrieved 2012-06-09

- 1 2 L Adkins, R A Adkins. Handbook to Life in Ancient Rome. Oxford University Press, 16 July 1998. ISBN 0195123328. Retrieved 2012-06-09.

- ↑ Charles F. Horne (1915). "The Code of Hammurabi : Introduction". Yale University. Retrieved 14 September 2007.

- ↑ Sheila C. Dow (2005), "Axioms and Babylonian thought: a reply", Journal of Post Keynesian Economics 27 (3), p. 385-391.

- ↑ The Reforms of Urukagina. History-world.org. Retrieved on 2011-02-10.

- ↑ J Parkhurst – A Greek and English Lexicon to the New Testament: In which the Words and Phrases ... are Distinctly Explained, and the Meanings Assigned to Each Authorized by References to Passages of Scripture, and Frequently ... Confirmed by Citations from the Old Testament and from the Greek Writers. To this Work is Prefixed, a ... Greek Grammar ... J Davis 1898 – Retrieved 2012-06-16

- ↑ J E Harrison – Epilegomena to the Study of Greek Religions and Themis a Study of the Social Origins of Greek Religion Kessinger Publishing, 1Jan 2003 ISBN 0766135284 Retrieved 2012-06-16

- ↑ secondary – Varro et al – Retrieved 2012-06-16

- ↑ D Sacks, O Murray A Dictionary of the Ancient Greek World Oxford University Press, 6 February 1997 ISBN 0195112067 Retrieved 2012-06-16

- ↑ secondary – The journal of the Royal Society of Antiquaries of Ireland 1894 " ...great treasury tombs probably range from this time to 1200..."

- ↑ J E Harrison – Themis: A Study of the Social Origins of Greek Religion Cambridge University Press, 24 June 2010 ISBN 1108009492 Retrieved 2012-06-16

- ↑ Roy Davies & Glyn Davies (3 June 2012). A Comparative Chronology of Money.

- ↑ G. Bailey, F. Law, M. Phillips (3 June 2012). Cowries, Coins, Credit: The History of Money. ISBN 0756516765.

- ↑ secondary (not showing statutes relevant) – A C Johnson, P Robinson Coleman-Norton, F C Bourne Ancient Roman Statutes: A Translation with Introduction, Commentary, Glossary, and Index Retrieved 2012-06-15

- ↑ C. Rollin, editor J. Bell – The Ancient History of the Egyptians, Carthaginians, Assyrians, Babylonians, Medes and Persians, Grecians, and Macedonians: Including a History of the Arts and Sciences of the Ancients, Volume 2 G. Dearborn, 1836 Retrieved 2012-06-17

- ↑ D Harper – Etymology online Retrieved 2012-06-17

- ↑ D S Evans, R Schmalensee – Paying with Plastic: The Digital Revolution in Buying and Borrowing MIT Press, 1 January 2005 ISBN 026255058X Retrieved 2012-06-17

- ↑ "attesting" – Cambridge Dictionary Online – Retrieved 2012-06-17

- ↑ I I Rubin, 'A History of Economic Thought', translated Donald Filtzer, Ink Links, 1979 (original Moscow, 1929)

- ↑ Biblos Retrieved 2012-05-04

- ↑ secondary – Jean Andreau (Director of Studies at the École pratique des hautes études, Paris). Banking and Business in the Roman World. Cambridge University Press, 14 October 1999. Retrieved 9 April 2012.

- ↑ secondary – Encyclopedia Britannica & French Dictionary (HarperCollins Publishers Limited 6 July 2010), Retrieved 2012-06-04

- ↑ F W Madden, F W Fairholt – History of Jewish coinage, and of money in the Old and New Testament B. Quaritch, 1864 Retrieved 2012-05-04

- ↑ J Free, H F Vos Archaeology and Bible History Zondervan, 15 September 1992 , ISBN 0310479614 – Retrieved 2012-06-04

- ↑ F N Magill, C J Moose Dictionary of World Biography: The Ancient World Taylor & Francis, 23 January 2003 ISBN 1579580408 Retrieved 2012-06-04

- ↑ I M Wise – History of the Israelitish nation: from Abraham to the present time J. Munsell, 1854 Retrieved 2012-06-04

- ↑ Madden & Fairholt

- 1 2 "The Jewish Virtual Library". American-Israeli Cooperative Enterprise. Retrieved 2012-06-04.

- ↑ Xenophon (translated by W Moyle) -Discourse on Improving the Revenue of the State of Athens – Retrieved 2012-06-09

- ↑ D Sacks, O Murray A Dictionary of the Ancient Greek World Oxford University Press, 1997 – Retrieved 2012-06-09

- ↑ secondary – – Retrieved 2012-06-09

- ↑ Greville Ewing – A Greek and English lexicon: originally a Scripture lexicon; and now adapted to the Greek classics; with a Greek grammar prefixed James Duncan, London 1827 (3rd Ed.) – Retrieved 2012-06-08

- ↑ L Kallet-Marx. Money, Expense, and Naval Power in Thucydides' History 1–5.24. University of California Press, 3 November 1993. ISBN 0520078209. Retrieved 2012-07-12.

- ↑ E Schiappa – Protágoras and Logos: A Study in Greek Philosophy and Rhetoric Univ of South Carolina Press, 2003 Retrieved 2012-07-12 ISBN 1570035210

- ↑ (secondary) -

- ↑ J Atwill – Rhetoric Reclaimed: Aristotle and the Liberal Arts Tradition Cornell University Press, 1998 Retrieved 2012-07-12 ISBN 0801432634

- ↑ A L Friedberg, I S Friedberg. Gold Coins of the World: From Ancient Times to the Present : an Illustrated Standard Catalog with Valuations. Coin & Currency Institute, 30 July 2009. ISBN 0871843080. Retrieved 2012-06-04.

- ↑ The bible Retrieved 2012-06-04

- ↑ C T Seltman. Athens, Its History and Coinage Before the Persian Invasion. CUP Archive, 1924. ISBN 0871843080. Retrieved 2012-06-04.

- ↑ Kramer, History Begins at Sumer, pp. 52–55.

- ↑ David Graeber: Debt: The First 5000 Years, Melville 2011. Cf. http://www.socialtextjournal.org/reviews/2011/10/review-of-david-graebers-debt.php Archived 10 December 2011 at the Wayback Machine.

- ↑ D Schaps, "The Invention of Coinage in Lydia, in India, and in China," paper presented at the XIV International Economic History Congress, Helsinki, 2006.

- ↑ Full text of "The earliest coins of Greece proper". archive.org. Retrieved on 2011-02-10.

- ↑ Coin images

- ↑ Ancient coinage of Aegina. snible.org. Retrieved on 2011-02-10.

- ↑ Goldsborough, Reid. "World's First Coin"

- ↑ http://hsc.csu.edu.au/ancient_history/societies/greece/spartan_society/sparta_social/ancient_sparta_socialsystem.htm

- 1 2 M M Postan, E Miller. The Cambridge Economic History of Europe: Trade and industry in the Middle Ages. Cambridge University Press, 28 August 1987. ISBN 0521087090.

- ↑ William Arthur Shaw. The History of Currency, 1252–1896. Library of Alexandria, 1967. ISBN 1465518878. Retrieved 2012-06-04.

- ↑ "Sir Isaac Newton's state of the gold and silver coin (25 September 1717).". Pierre Marteau.

- ↑ "Mineral Profiles" (PDF). U.S. Geological Survey.

- ↑ Davies, Glyn, ‘’A History of Money’’, University of Wales, 1994, p.172, 339. ISBN 0-7083-1717-0

- ↑ Davies, Glyn, ‘’A History of Money’’, University of Wales, 1994, pp. 146–151 ISBN 0-7083-1717-0

- ↑ Richards

- ↑ Thus by the 19th century we find “[i]n ordinary cases of deposits of money with banking corporations, or bankers, the transaction amounts to a mere loan or mutuum, and the bank is to restore, not the same money, but an equivalent sum, whenever it is demanded.” Joseph Story, Commentaries on the Law of Bailments (1832, p. 66) and “Money, when paid into a bank, ceases altogether to be the money of the principal (see Parker v. Marchant, 1 Phillips 360); it is then the money of the banker, who is bound to return an equivalent by paying a similar sum to that deposited with him when he is asked for it.” Lord Chancellor Cottenham, Foley v Hill (1848) 2 HLC 28.

- ↑ Richards. The usual denomination was 50 or 100 pounds, so these notes were not an everyday currency for the common people.

- ↑ Richards, p. 40

- ↑ Daniel R. Headrick (1 April 2009). Technology: A World History. Oxford University Press. pp. 85–. ISBN 978-0-19-988759-0.

- ↑ Ebrey, Walthall, and Palais (2006), 156.

- ↑ Bowman (2000), 105.

- ↑ Gernet (1962), 80.

- ↑ Ebrey et al., 156.

- ↑ Gernet, 80.

- ↑ Moshenskyi, Sergii (2008). History of the weksel: Bill of exchange and promissory note. p. 55. ISBN 978-1-4363-0694-2.

- ↑ Marco Polo (1818). The Travels of Marco Polo, a Venetian, in the Thirteenth Century: Being a Description, by that Early Traveller, of Remarkable Places and Things, in the Eastern Parts of the World. pp. 353–355. Retrieved 19 September 2012.

- ↑ The Alchemists: Three Central Bankers and a World on Fire - Neil Irwin - Google Books

- ↑ De Geschiedenis van het Geld (the History of Money), 1992, Teleac, page 96

- ↑ Geisst, Charles R. (2005). Encyclopedia of American business history. New York. p. 39. ISBN 978-0-8160-4350-7.

- ↑ Karl Gunnar Persson – An Economic History of Europe: Knowledge, Institutions and Growth, 600 to the Present Cambridge University Press, 28 January 2010 , ISBN 052154940X – Retrieved 2012-06-03

Bibliography

- Bowman, John S. (2000). Columbia Chronologies of Asian History and Culture. New York: Columbia University Press. ISBN 0231110049

- Ebrey, Walthall, Palais, (2006). East Asia: A Cultural, Social, and Political History. Boston: Houghton Mifflin Company. ISBN 0618133844

- Del Mar,A A History of Money in Ancient Countries from the Earliest Times to the Present

- Gernet, Jacques (1962). Daily Life in China on the Eve of the Mongol Invasion, 1250–1276. Stanford: Stanford University Press. ISBN 0-8047-0720-0

- Richards, R. D. Early history of banking in England. London: R. S. King, 1929.

Further reading

- Alvarado, Ruben, Follow the Money: The Money Trail Through History, WordBridge 2013.

- Jevons, W. S. (1875), Money and the Mechanism of Exchange. London: Macmillan.

- Menger, Carl, "On the Origin of Money"

- Szabo, Nick, Shelling Out – The Origins of Money

- Weatherford, Jack (1997), The History of Money. New York: Crown Publishers.

External links

| Wikimedia Commons has media related to Money. |

- The Marteau Early 18th-Century Currency Converter A Platform of Research in Economic History.

- Linguistic and Commodity Exchanges by Elmer G. Wiens. Examines the structural differences between barter and monetary commodity exchanges and oral and written linguistic exchanges.

- Historical Currency Conversion Page by Harold Marcuse. Focuses on converting German marks to US dollars since 1871 and inflating them to values today, but has much additional information on the history of currency exchange.

{kind=link}